Managing Personal Finances

The talk on managing finances was delivered by Mr Stephen Chin in SCIC on Sunday, 18th August 2019.

Financial wellness is living within one’s means and learning to manage one’s finances for the short and long term. It is characterised by the following four pillars:

- Living within one’s means

- Wisdom to make good financial decisions

- Being financially prepared for emergencies

- Having a plan for the future

There are several basic principles that one should pay attention to in ensuring financial wellness:

Income. God provides opportunities to receive provisions directly or indirectly from His hands. Having a source of income is essential to sustain the necessities of day-to-day living.

Cashflow. Always spend less that what is earned. Manage spending by planning ahead. A variety of digital applications are available that can help to manage and keep track of expenses. Avoid impulsive purchases – make a list of items needed before a trip to the store and use a basket instead of a trolley when shopping.

Lifestyle. Lead a simple lifestyle and practice contentment. When deciding on purchases including, food, clothes, car, and holiday, go back to the objective of having the object. An expensive holiday does not make it more enjoyable than an affordable one. Evaluate needs versus wants and spend prudently.

Debt. Manage credit card debts by paying it off in full amounts monthly instead of only making the minimum payment requirement. Keep track of other debts such as, housing, car and study loans by obtaining a personal credit report (https://www.ramcreditinfo.com.my/). This can be used to improve one’s credit status. Limit debt to income generating assets. Don’t hesitate to seek professional help from Agensi Kaunseling dan Pengurusan Kredit for assistance on debt restructuring and rescheduling.

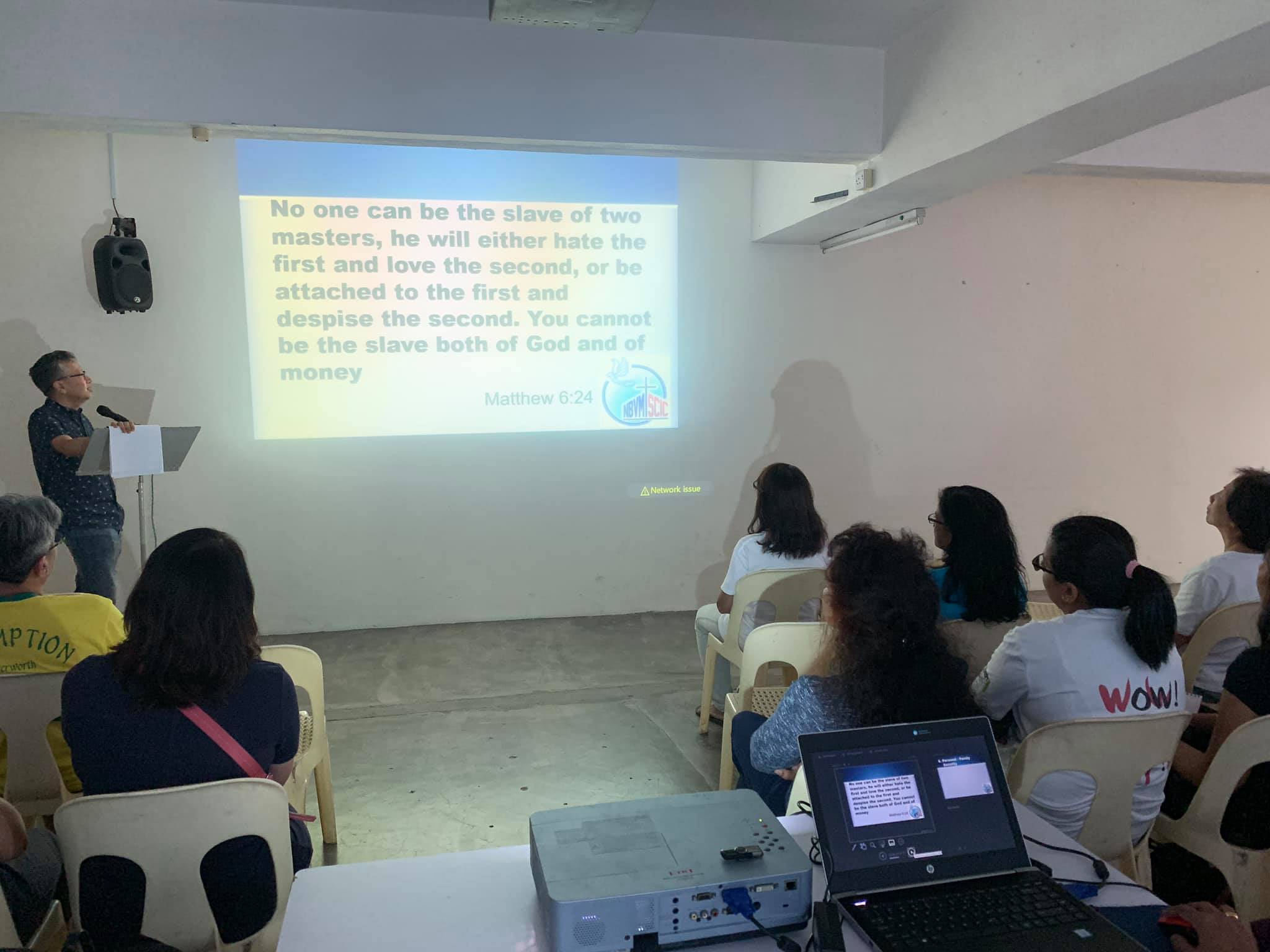

Investment. Investment is helpful to diversify one’s income, however, as Christians we are reminded to be prudent in gathering wealth and to never hoard. Avoid get-rich-quick schemes – a list of fraudulent companies and schemes can be obtained from http://www.bnm.gov.my/index.php?lang=en&ch=en_financialconsumeralert When planning to invest, understand the concept of liquidity in investment. The most liquid types of investment are fixed deposits and unit trust. Property purchases are low in risk but not liquid, while purchase of shares may be risky and needs thorough analysis of trends. Cryptocurrency is currently the buzz and may provide good returns, however, as they are a relatively new asset much remains unknown and it is also not recognized by all central banks.

Security. Having sufficient savings and proper insurance coverage are essential for security in difficult times. Make contingency plans for the unexpected such as, unemployment, accident, and medical issues. Plans for a comfortable retirement should also be put in place. This may involve moving from a larger house to a smaller one once children have moved out of the house – not a down-sizing, rather right-sizing according to present circumstances.

Finally, equally important is to remember to also give to those who are in need. Whoever cares for the poor lends to the Lord, who will pay back the sum in full. (Proverbs 19:17) A point worth noting when giving is that organizations which use intermediaries to appeal for funds such as the National Kidney Foundation, Worldwide Fund for Nature (WWF) and UNICEF (often seen in shopping malls and other public places) would need to allocate a portion of the funds donated to pay the intermediaries. Therefore, opt to directly donate to the organizations rather than going through these third parties.

Security tips for online transactions

- Use strong security pins and change them regularly – a combination of numbers, alphabets and special characters. Do not use birth dates, car registration or other easily identifiable numbers.

- Pay attention to surroundings when keying-in pin

- Ensure devices are locked

- Remember to log out of accounts

- Check transactions and statements regularly

- Update software and applications in a timely manner

- Install anti-virus

- Do not use public internet connections to do banking transactions

(by Kathlin Ambrose)